Why Trademark Registration is Crucial for Your Startup's Growth

Are you dreaming of launching your startup without relying on external funding? Learn how to bootstrap your startup with these essential tips. From using affordable tools to finding the perfect mentor, this guide will help you build a successful and self-sustaining business. Dive in and turn your entrepreneurial dreams into reality!

💡Did You Know?

Source: Gitnux [1]

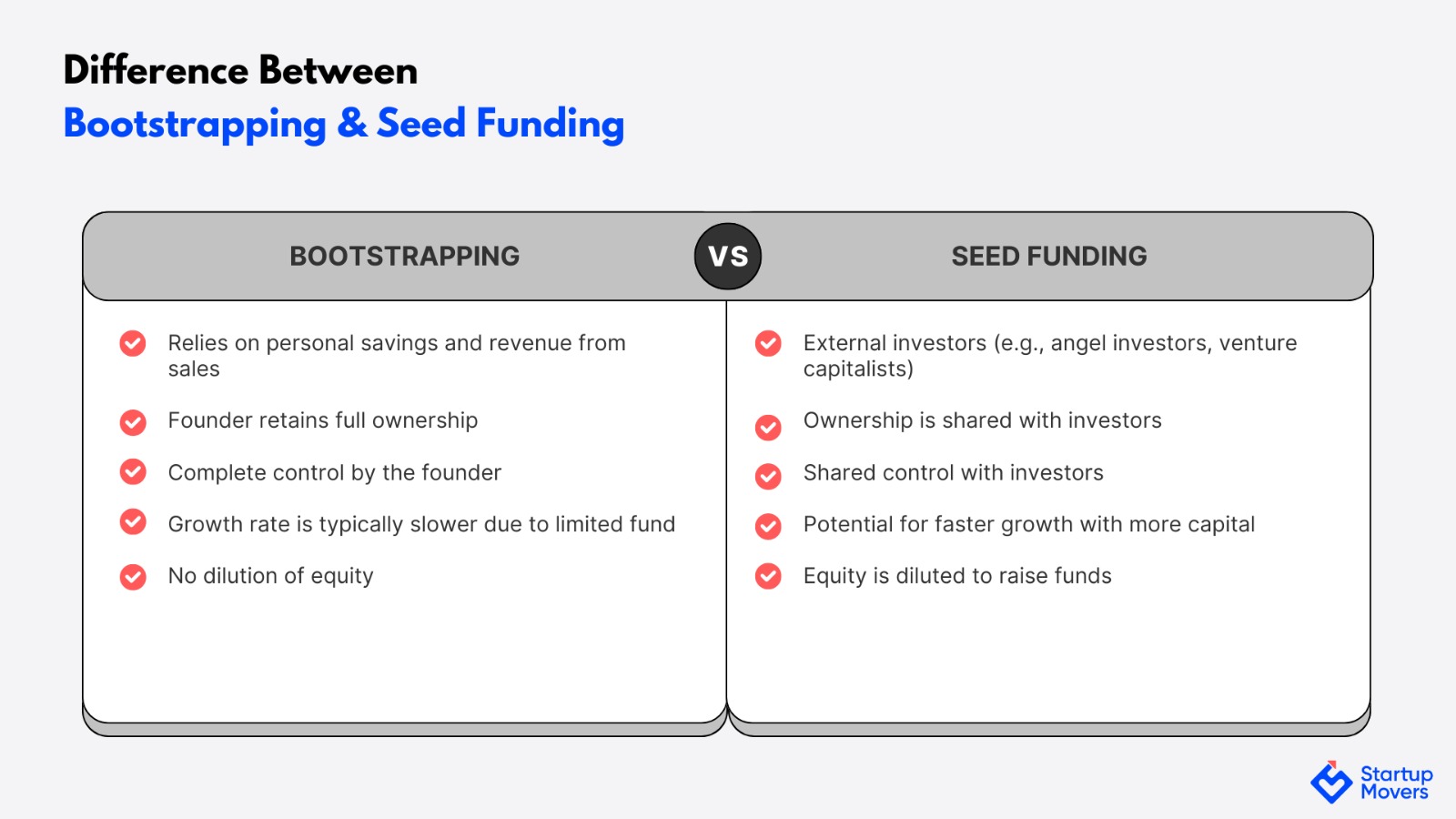

Bootstrapping your startup means starting and growing your business using your own money or the revenue it generates. No investors, no loans—just your hard-earned cash and a whole lot of determination. This approach lets you keep full control over your startup and is all about being smart with your resources, staying creative, and focusing on generating cash flow quickly.

Seed funding is when you raise initial capital from investors, which can give your business a good boost but often requires giving up equity and meeting investor demands.

Bootstrapping, on the other hand, relies on personal savings and revenue reinvestment. It’s all about keeping ownership and control but demands careful financial management and a knack for resourcefulness.

Here are some essential tips to help startups effectively bootstrap their way to success.

Before you pour time and money into your project, make sure there’s a real market need. Talk to potential customers, run surveys, and gather feedback. This step helps you avoid costly mistakes and ensures you’re building something people actually want.

Keep your costs down by using free or affordable tools. Platforms like Trello for project management, MailChimp for email marketing, and Canva for design can help you manage your business without spending a fortune.

Focus on what you do best and outsource or automate the rest. Websites like Upwork and Fiverr can connect you with freelancers for tasks like graphic design and content writing. Automation tools like Zapier can handle repetitive tasks, saving you time and money.

Show that there’s demand for your product or service as early as you can. Whether it’s through gaining your first customers, generating revenue, or building user engagement. Proving traction validates your business model and can attract partners or customers.

One of the biggest decisions you’ll make is whether to go it alone or find a co-founder. A co-founder can bring complementary skills, share the workload, and provide support during tough times. Make sure they share your vision and values to avoid conflicts down the road.

Hiring full-time executives can be pricey. Consider using fractional CXO services like virtual CFOs or part-time CMOs. These professionals offer strategic guidance without the high cost of full-time hires.

Get top-tier financial guidance without the full-time cost with our virtual CFO services.

Stay flexible and be ready to change your business model if needed. Listen to market feedback and be willing to pivot based on what you learn. This adaptability can be key to finding success.

Don’t get distracted by vanity metrics like social media followers. Focus on metrics that really matter, like customer acquisition cost, lifetime value, and conversion rates. These give you a clearer picture of your business’s health.

Choosing the right business structure is important for legal and financial reasons. For bootstrapped startups, incorporating as a Limited Liability Partnership (LLP) can be a smart move, offering limited liability and operational flexibility. Consult with a legal professional to decide what’s best for you.

Get expert help to incorporate your business as an LLP and enjoy the benefits of limited liability and flexibility

A mentor can offer invaluable advice and insights. Look for experienced entrepreneurs or professionals who’ve been through the challenges you’re facing. Platforms like SCORE or local business networks can help you find a mentor who aligns with your goals.

Keeping a close eye on your expenses is crucial. Use accounting software like QuickBooks or Xero to track your finances and create detailed budgets. Regularly review your financial statements to make sure you’re staying on track.

Let our expert bookkeeping services handle the numbers, so you can focus on your startup’s growth.

Invest in your brand and content marketing to boost your startup’s visibility. Develop a strong brand identity with a memorable logo and compelling story. Use content marketing strategies like blogging, social media, and email marketing to engage your audience. Zoho, a successful bootstrapped startup in India, used content marketing to grow its brand globally without external funding.

Networking can be a game-changer for bootstrapped entrepreneurs. Attend industry events, join online communities, and connect with other entrepreneurs. Networking can lead to valuable partnerships, customer referrals, and collaboration opportunities that help your startup thrive.

Bootstrapping allows you to retain full ownership, make independent decisions, and encourages efficient use of resources. It also reduces financial risk and fosters innovation.

Bootstrapping a startup means building and growing the business using personal savings, revenue from initial sales, and minimal external funding.

The main disadvantages include limited resources, slower growth, increased financial pressure on founders, and potential challenges in scaling the business.

The success rate of bootstrapping varies widely, but many successful companies, like Mailchimp and Spanx, started this way. Specific statistics can be hard to pin down due to varying definitions of success.

Bootstrapping your startup is all about being resourceful, planning strategically, and staying determined. Follow these tips to build a strong foundation and increase your chances of success without relying on external funding. Remember, every decision you make shapes your startup’s future. Stay focused, stay resilient, and watch your entrepreneurial dreams come to life.

© 2025 Startup Movers Private Limited. All rights reserved. | Designed By : The Night Marketer