Startups increasingly opt for an India-US setup to leverage global markets, talent, and investors. However, founders face challenges like complex regulations, dual taxation, and operational hurdles. Discover how a cross-border startup setup can drive growth.

Our latest blog is here to guide your India-US startup journey!

In today’s rapidly evolving business landscape, the India-US startup setup has emerged as a strategic choice for entrepreneurs seeking to tap into global markets.

This setup involves establishing a business presence in both India and the United States, enabling startups to leverage the strengths of each country.

By combining India’s vast pool of tech talent and cost-effective operational advantages with the US’s access to capital and innovative ecosystems, startups can position themselves for significant growth and success.

The India-US setup typically entails registering a company in one or both countries, complying with local regulations, and navigating tax implications and adhering to the Foreign Exchange Management Act (FEMA) in India, which governs foreign investments and currency exchange.

In summary, establishing an India-US startup setup is not just about geographical presence; it’s about leveraging the unique advantages of both markets to drive growth, attract investment, and foster innovation.

The rise of the India-US startup setup is significant, with Indian founders establishing a prominent presence in the U.S. market.

|

Over 55% of billion-dollar startups in the U.S. have immigrant founders, with Indians at the forefront, founding 66 such companies according to a recent National Foundation for American Policy (NFAP) report. |

Moreover, the COVID-19 pandemic accelerated digital transformation, enabling startups to operate effectively across borders. A report from McKinsey & Company indicates that 75% of businesses have adopted digital tools, making cross-border collaboration more feasible than ever.

The rising trend of India-US setups among startups can be attributed to several key factors:

Discover the Opportunities, Steps, and Compliance Essentials for Expanding Your Startup Across Borders

Get Started TodayIn an India-US setup, the holding subsidiary structure can be established in either direction, allowing for flexibility in international business operations.

The India-US holding-subsidiary model involves a parent company in either the U.S. or India owning a significant stake in a subsidiary located in the other country. It involves:

When Indian startups consider establishing a presence in the US, they often choose from several common legal structures, each offering unique benefits and regulatory implications.

Below table summarizes the popular structures along with their advantages and disadvantages:

|

Legal Structure |

Advantages |

Disadvantages |

|

Limited Liability Company (LLC) |

- Combines partnership flexibility with corporation liability protection. - Pass-through taxation. |

- May face challenges attracting venture capital. - More complex to manage than a sole proprietorship. |

|

C-Corporation (C-Corp) |

- Preferred by investors; can issue multiple classes of stock. - Limited liability protection. |

- Subject to double taxation. - Higher regulatory compliance costs. |

|

S-Corporation (S-Corp) |

- Pass-through taxation, avoiding double taxation. - Limited liability protection. |

- Limited to 100 shareholders, all must be U.S. citizens or residents. |

|

Partnership |

- Easy to form; offers pass-through taxation. |

- General partners share liability for business debts. - Limited liability partnerships may have ownership restrictions. |

|

Non-Profit Organisation |

- Can qualify for tax-exempt status; able to attract donations. |

- Must adhere to strict regulations regarding profit distribution and transparency. |

|

Single Person Business |

- Simple to establish and manage; full control of business decisions. - Pass-through taxation. |

- Personal liability for business debts; harder to raise funds compared to other structures. |

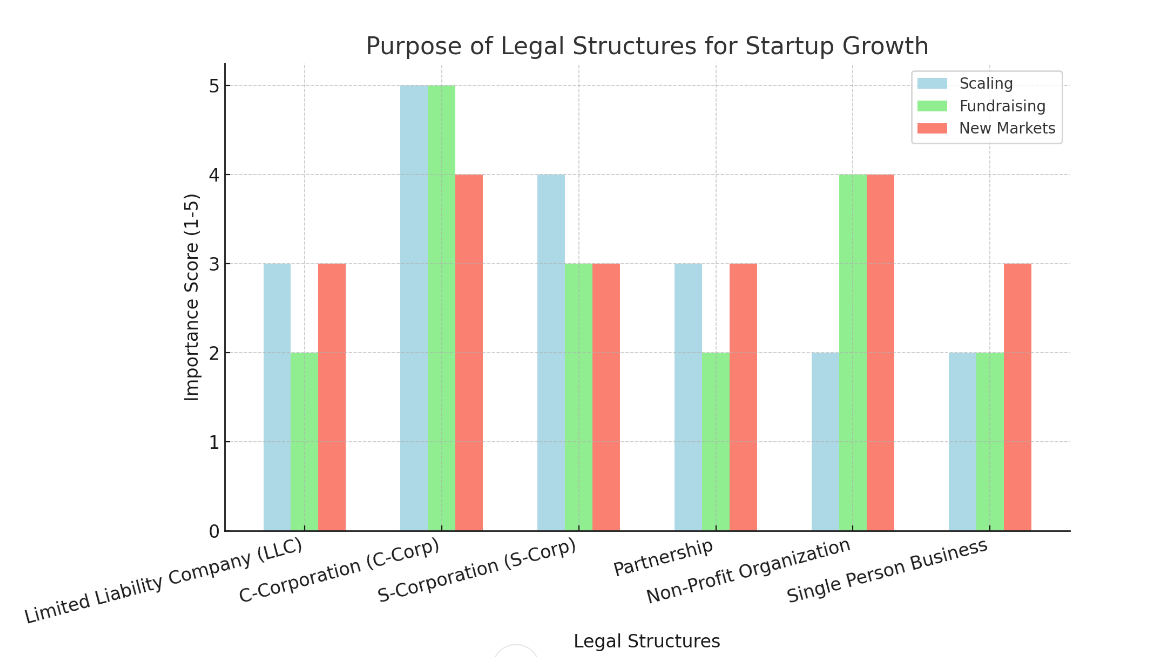

LLCs and C-Corps enable rapid scaling and access to extensive fundraising opportunities while facilitating entry into new markets. In contrast, S-Corps, partnerships, and single-person businesses offer limited scalability and fundraising options, with varying potential for market expansion.

Refer to the table and graph below for further insights and comparisons.

The graph depicts the varying degrees of importance that different legal structures hold for startups, highlighting that C-Corps and LLCs are the most advantageous for scaling and fundraising, while also facilitating entry into new markets.

Challenges can be particularly daunting for startups due to the differing legal frameworks, procedures, and requirements in each country. Here are some specific legal and regulatory challenges that founders may encounter:

Startups expanding into both India and the U.S. face various administrative and operational hurdles that can complicate their growth. Key challenges include:

Startups operating in both India and the U.S. face the challenge of complying with differing financial reporting standards.

In India, companies must adhere to Indian Accounting Standards (Ind AS), while in the U.S., they must follow Generally Accepted Accounting Principles (GAAP).

This dual compliance requires careful coordination, as reporting timelines, formats, and audit requirements vary, making financial management complex and resource-intensive.

Let Us Lighten Your Load - Discover expert insights and support to navigate the complexities of your India-U.S. startup journey!

Find Out HowTransfer pricing regulations in both India and the U.S. require that cross-border transactions between related entities be conducted at arm's length.

In India, startups must comply with the Income Tax Act, 1961, which mandates detailed documentation for all intercompany transactions and periodic audits. In the U.S., the Internal Revenue Code requires similar arm's length pricing, with strict penalties for non-compliance.

Startups must ensure accurate pricing of goods, services, and intellectual property to avoid hefty fines and adjustments in both countries.

Here's a comparison table outlining the key Transfer Pricing (TP) requirements for India and the US:

|

Requirement |

India |

United States |

|

Applicable Law |

Income Tax Act, 1961 (IITA) |

Internal Revenue Code (IRC) |

|

Key Authority |

Indian Tax Authorities |

Internal Revenue Service (IRS) |

|

Arm’s Length Principle |

Required for cross-border transactions |

Required for intercompany transactions |

|

Documentation Requirements |

- Master File - Country-by-Country Report (CbCR) for groups with revenue > ₹6,400 crore |

- Contemporaneous documentation for all major transactions |

|

Audits & Enforcement |

Tax authorities conduct audits and adjustments |

IRS enforces with potential audits and adjustments |

|

Advanced Compliance Mechanism |

N/A |

Advance Pricing Agreements (APAs) available |

|

Non-Compliance Penalties |

Significant penalties for failure to comply |

Strict penalties for non-compliance and potential adjustments |

Transfer pricing methods: Includes Comparable Uncontrolled Price (CUP), Cost Plus, Resale Price, Profit Split, and Transactional Net Margin Method (TNMM), ensure arm's length pricing for intercompany transactions by comparing controlled transactions to market benchmarks or allocating profits based on the relative contributions of each party involved.

Non-Compliance Risks: Non-compliance can lead to significant penalties, tax adjustments, and reputational damage, often due to inadequate documentation or improper method application.

Choosing the right transfer pricing method is essential. Companies should consider factors like the nature of transactions, availability of comparables, and market conditions to mitigate compliance risks and optimize their tax positions.

Foreign Direct Investment (FDI) refers to an investment made by an individual or entity in one country in business interests in another country, typically in the form of establishing business operations, acquiring assets, or investing in joint ventures.

Overseas Direct Investment (ODI) refers to investments made by Indian companies in foreign countries, enabling them to establish or expand business operations beyond India. This can include acquiring assets, setting up subsidiaries, or forming joint ventures abroad.

Navigating Foreign Direct Investment (FDI) and Overseas Direct Investment (ODI) in an India-U.S. setup poses significant challenges for startups.

They must contend with complex regulatory frameworks, sector-specific restrictions, and rigorous compliance requirements while addressing tax implications under the Double Taxation Avoidance Agreement (DTAA), necessitating a proactive and informed approach.

Establishing a business presence in the U.S. from India presents startups with a complex array of visa and immigration challenges.

Startups must choose the appropriate visa, such as H-1B for skilled workers, L-1 for intra-company transfers, and O-1 for individuals with extraordinary abilities. The L-1 visa necessitates proof of a qualifying relationship between companies, demanding careful documentation.

To navigate an India-U.S. startup setup, founders should conduct market research, choose the right business structure, and maintain clear communication. Emphasizing legal compliance and strong HR practices while leveraging technology and local networks will enhance collaboration and drive growth.

Expert knowledge of complex tax regulations and strategies for minimizing liabilities helps navigate challenges like double taxation and transfer pricing, allowing you to concentrate on growing your business.

It guarantees fair pricing of intercompany transactions, ensures compliance, and reduces audit risks. By prioritizing this, you enhance operational efficiency and foster trust with tax authorities, paving the way for long-term success.

Efficiently managing operational challenges

It involves strong communication, efficient processes, and understanding cultural differences. By leveraging local knowledge and technology, startups can streamline operations and navigate regulatory complexities.

Their expertise ensures compliance with local regulations, protects intellectual property, and streamlines contract negotiations. This partnership helps mitigate legal risks, enabling startups to focus on growth and innovation.

Establishing a startup across the India-U.S. landscape is a thrilling opportunity to create a bridge between two vibrant markets. By mastering the legalities, tax structures, and cultural differences, you're not just building a business—you're driving innovation and collaboration.

Turn challenges into opportunities for growth and see your vision succeed. Ready to start your journey? Get connected with us for your India-U.S. startup today!"From financial compliance to growth strategy, we’ve got you covered.

Get on a 1:1 call with usQ. Can an Indian start a startup in the USA?

Yes, an Indian can start a startup in the USA by choosing a suitable business structure, registering the business, securing the necessary visa, and ensuring compliance with local regulations. This venture offers access to a larger market and growth opportunities.

Q. What is a holding-subsidiary structure in the context of an India-US startup setup?

A holding-subsidiary structure in an India-US startup setup consists of a parent company (holding company) that owns and controls one or more subsidiaries in each country, enabling centralized management, risk mitigation, and potential tax benefits while facilitating market access in both regions.

Q. How does the Double Taxation Avoidance Agreement (DTAA) benefit India-US startups?

The Double Taxation Avoidance Agreement (DTAA) allows India-US startups to avoid being taxed on the same income in both countries, facilitating easier profit repatriation and reducing their overall tax liability.

© 2026 Startup Movers All rights reserved. | Designed By : The Night Marketer

Leave a Comment

Comments

No comments yet.

RECENT ARTICLES

Difference Between GSTR-9 & GSTR-9C

Share Purchase Agreement: Complete Founder’s Guide 2026

Why Trademark Registration is Important for Businesses in India

Difference Between ESOP & SAR: Employee Compensation Plan

From Idea to IPO: How Women Are Owning the Startup Game

Organizational Digital Signature Certificate (DSC): Complete Guide

GST Update: Withdrawal from Rule 14A through form GST REG-32

Difference Between LLP & Private Limited Company