Understanding Softex Filings

Navigating SaaS compliance in India can be overwhelming, with intricate regulations on GST on SaaS exports and TDS on software services. Understanding SaaS GST rules in India is crucial to avoid penalties and ensure smooth operations. This guide will clarify these complexities and streamline your compliance journey.

Ready to simplify your SaaS tax compliance? Read on for key insights!

Before we navigate the SaaS compliances in India, let’s quickly look at what are SaaS based Companies:

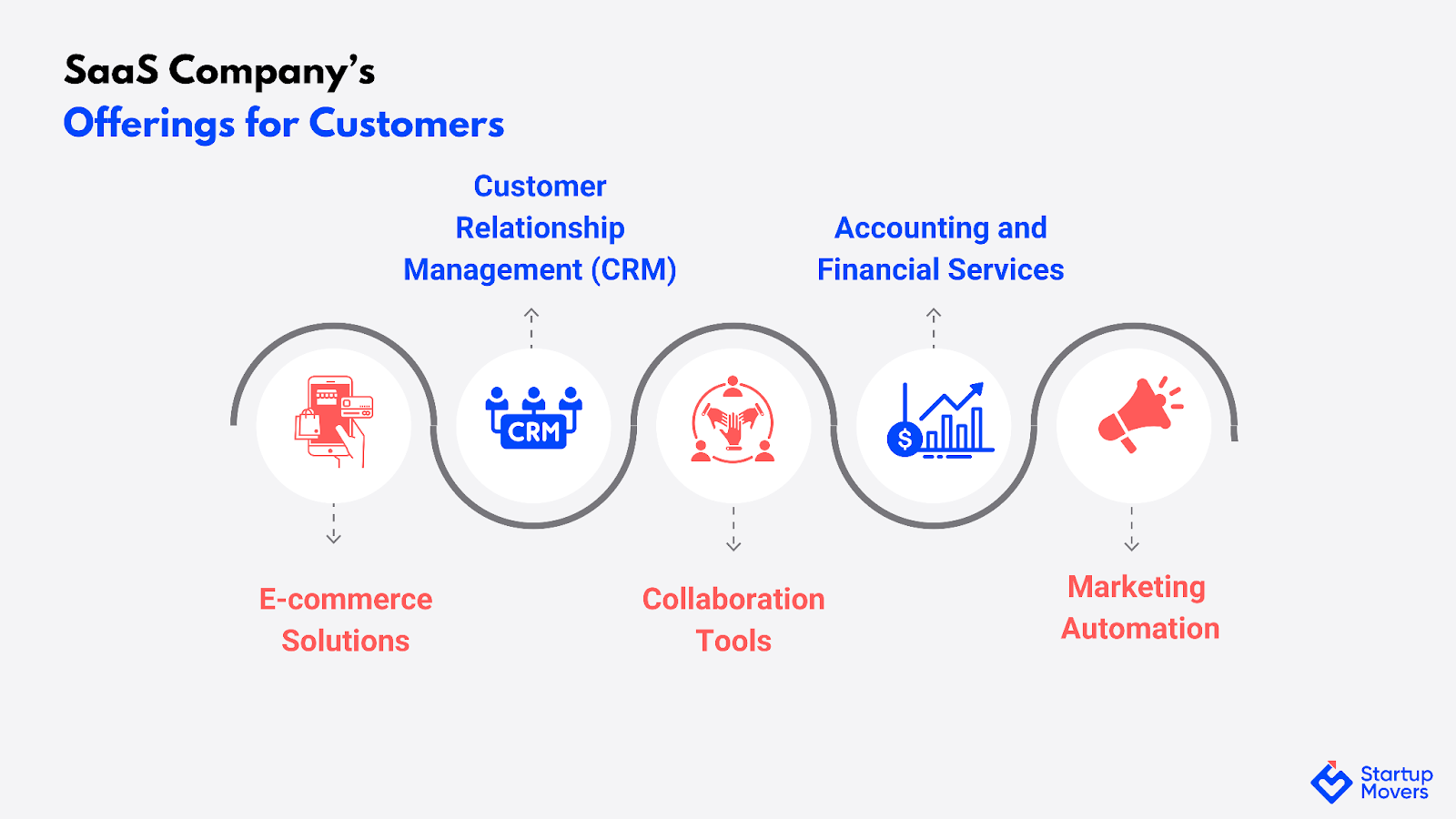

SaaS companies offer a wide range of services tailored to meet the diverse needs of their customers. Some common offerings include:

The landscape of SaaS (Software as a Service) in India is increasingly influenced by the regulatory framework surrounding GST (Goods and Services Tax).

GST implications for SaaS services differ based on whether the provider is an Indian or a foreign company.

SaaS services fall under the definition of Online Information and Database Access or Retrieval (OIDAR) services.

|

OIDAR services include services delivered over the internet that are essentially automated and require minimal human intervention. SaaS fits into this category as it provides software access via the internet. |

According to the IGST Act, the place of supply for SaaS is the recipient's location. Thus, foreign SaaS providers delivering services to Indian customers must obtain GST registration in India and comply with local regulations, including filing returns.

Understanding these rules and complying with OIDAR regulations is crucial for both types of providers to ensure seamless operations within the GST framework.

SaaS products fall under specific HSN (Harmonized System of Nomenclature) codes for GST classification. Generally, the HSN code for software services is 9983, and these services typically attract an 18% GST rate. However, it’s vital to check for updates or amendments to these rates, as the regulatory landscape may evolve.

Every SaaS business in India must obtain GST registration if their annual turnover exceeds ₹20 lakhs (₹10 lakhs for special category states). Registration not only ensures compliance but also enables businesses to claim input tax credits (ITC) on GST paid for inputs and services used.

SaaS companies are required to follow specific invoicing guidelines under GST. The introduction of e-invoicing mandates businesses with a turnover exceeding ₹5 crores to generate electronic invoices for their B2B transactions. Compliance with these regulations simplifies filing and helps avoid discrepancies.

Input Tax Credit (ITC) is a significant benefit for SaaS providers, allowing them to reduce their tax liability. To be eligible for ITC, companies must ensure that the inputs and services purchased are used to provide taxable supplies. The claiming process involves filing monthly returns, maintaining records, and ensuring proper documentation.

SaaS exports are categorized as zero-rated supplies under GST, meaning that exporters do not have to pay GST on exported services. This zero-rating also allows for the claim of refunds on the GST paid for inputs used in providing exported services. Exporters must file a Letter of Undertaking (LUT) to facilitate this process.

Software categorized under HSN Code 997331 is recognized as a service import. Importers, whether companies or individuals, are not required to file a Bill of Entry for these services.

Instead, they must remit the applicable Integrated Goods and Services Tax (IGST) through the Reverse Charge Mechanism (RCM), in accordance with Notification 10/2017-IT issued in June 2017.

This tax payment is recorded in GSTR-1, allowing the importer to claim Input Tax Credit (ITC), which will then be reported in GSTR-3B.

Tax Deducted at Source (TDS) is another crucial area for SaaS companies. Understanding the TDS implications for both Indian and foreign SaaS companies is essential for compliance.

For Indian SaaS companies, TDS must be deducted at specified rates on payments made for software services. The standard TDS rate for SaaS companies is 10%, and companies must ensure timely deductions and remittances to avoid penalties.

Section 195 & Supreme Court Ruling (2021)

Section 195 requires any Indian entity making payments to a non-resident to deduct tax if the income is taxable in India, typically applicable to royalties or fees for technical services.

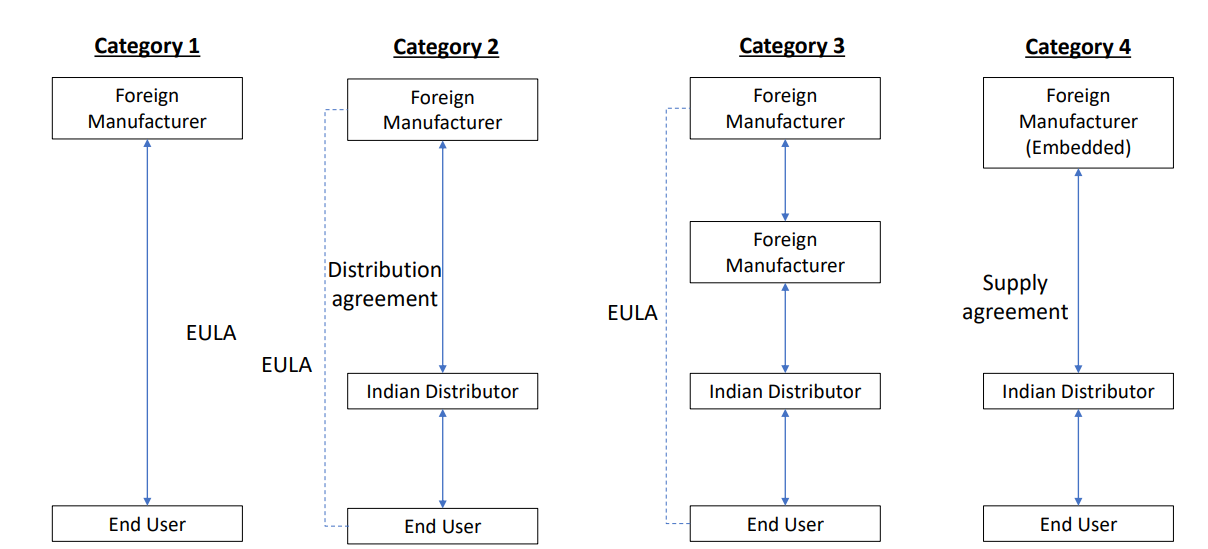

In the Supreme Court ruling of 2021, in the case of Engineering Analysis Centre of Excellence Pvt. Ltd. vs. Commissioner of Income Tax, which was decided on March 2, 2021 a key issue was whether payments for software licences to foreign companies should be treated as ‘royalties’ under Section 195, requiring TDS deductions.

Several appeals were combined, addressing software purchases like embedded software, server access, and licensing agreements. Below chart presents all the four categories discussed by the Supreme Court:

Source: ctconline.org, EULA is “End-User Licensing Agreement.

The Court ruled that these payments were not considered royalties, as the Indian company was purchasing software, not rights to reproduce or modify it.

Consequently, these payments did not attract TDS under Section 195, as these do not constitute income that is taxable in India providing significant relief for Indian companies dealing with foreign software vendors.

Importance of DTAA

Double Taxation Avoidance Agreements (DTAA) play a vital role in determining TDS rates on payments to foreign companies. Under DTAA, the TDS rate may be reduced, enabling Indian companies to mitigate tax liabilities when paying foreign SaaS providers.

Removal of Equalisation Levy in Budget 2024

The Equalisation Levy, introduced in India in 2016, targeted foreign digital companies, imposing a 6% tax on online advertisements and later a 2% tax on e-commerce transactions, including Software as a Service (SaaS).

The 2024 Union Budget abolished the 2% Equalisation Levy on e-commerce, effective August 1, 2024, to simplify compliance for foreign companies.

The decision to eliminate the Equalisation Levy reflects India's commitment to simplifying its tax regime for foreign digital service providers, making it easier for SaaS companies to thrive and expand in the Indian market .

SaaS companies in India face challenges with transfer pricing in cross-border deals. Transfer pricing sets prices for transactions within a group of related companies. This is crucial for fair pricing and tax compliance.

SaaS companies often rely on intangibles, R&D, and shared costs. These factors make transfer pricing tricky. This section covers key issues and offers simple solutions based on case laws.

Transfer Pricing Challenges and Solutions for SaaS Companies in India

|

Transfer Pricing Issue |

Recommendation & Case Law |

|

Intangibles and Transfer Pricing |

Ensure appropriate compensation for the use of intangibles by reflecting the economic value created in intercompany transactions, as highlighted in the CIT v. Samsung Electronics Co. Ltd. [2011] case. |

|

Contract R&D Services |

Conduct a functional and risk analysis to determine arm's length pricing for R&D services, aligning with economic substance, as demonstrated in Google India Private Limited v. Deputy Commissioner of Income Tax [2017]. |

|

Cost Contribution Arrangements (CCAs) |

Use a detailed functional analysis to allocate costs and benefits based on actual functions, risks, and assets utilized, as advised in Citrix Systems Asia Pacific Pty Ltd v. Commissioner of Income Tax [2010]. |

|

Transfer Pricing Methods |

Select the most appropriate transfer pricing method based on a comparability analysis and ensure consistent application throughout, as reinforced in ADIT v. Aztec Software and Technology Services Ltd [2007]. |

|

Documentation and Penalties |

Maintain comprehensive documentation to substantiate transfer pricing policies and avoid penalties; this was underscored in Director of Income Tax v. Quark Systems Pvt. Ltd. [2015]. |

|

Advance Pricing Agreements (APAs) |

Enter into APAs to predefine transfer pricing methods and avoid disputes, following the approach validated by Honda Siel Power Products Ltd v. Commissioner of Income Tax [2013], which promotes a cooperative tax environment and reduces transfer pricing risk. |

SOFTEX compliance is essential for Indian software exporters to ensure legal monitoring of foreign exchange earnings. The Reserve Bank of India (RBI) requires all software export declarations to be made using the SOFTEX Form, which records export value and tracks inward remittance of foreign earnings.

This compliance process ensures that companies meet regulatory standards and allows for accurate reporting of software export income. The filing of SOFTEX Forms must be timely, as delays can result in penalties or scrutiny from regulatory bodies.

Companies typically submit these forms to the Software Technology Parks of India (STPI) or Special Economic Zone (SEZ) authorities. Following SOFTEX guidelines protects businesses from regulatory risks and helps maintain smooth, compliant export operations.

Indian SaaS companies must adhere to Ind AS 115, which outlines how revenue from contracts with customers should be recognized. This standard aligns with IFRS 15 and focuses on recognizing revenue when performance obligations are met.

SaaS businesses need to account for their diverse revenue streams, depending on the business model they follow. Below are key models for revenue recognition in SaaS companies:

In the subscription model, customers pay periodically (monthly or annually) to access the software. Revenue is recognized over time, as the service is provided continuously throughout the subscription period. For instance, if a customer subscribes for a year, the revenue is recognized evenly over the 12 months.

However, if the payment is received upfront, the entire amount is initially recorded as deferred revenue and gradually recognized as revenue over the course of the subscription, ensuring compliance with revenue recognition standards like Ind AS 115. This ensures that revenue is only recognized when the services are actually delivered.

In cases where SaaS companies offer multiple services or deliverables as part of a contract (e.g., software, training, and customer support), revenue is allocated to each performance obligation based on its standalone selling price. Revenue is recognized as each distinct service or obligation is fulfilled.

Some SaaS contracts may include performance-based pricing or other variables, such as usage-based fees. In this case, companies must estimate the amount of variable consideration that is likely to be collected. Revenue is recognized only when it's highly probable that no significant reversal will occur when the uncertainty is resolved.

SaaS companies often charge upfront fees for services such as implementation or setup. These fees are typically deferred and recognized as revenue over the term of the customer contract. Deferred revenue (liabilities on the balance sheet) represents money received but not yet earned, and it is recognized once the related services are provided.

Many SaaS companies offer free trials to attract customers. No revenue is recognized during the trial period. Revenue recognition begins only when the customer converts to a paid subscription, and it follows the subscription-based model, recognizing revenue over the subscription term.

SaaS compliance in India encompasses various aspects, from GST and TDS to revenue recognition. By understanding the nuances of these regulations, SaaS businesses can navigate the complexities of compliance, ensuring smooth operations and reducing the risk of penalties. Adopting best practices for tax compliance will not only streamline operations but also enhance business credibility.

For tailored assistance, consider engaging with compliance experts who can guide you through the intricacies of SaaS tax compliance in India.

Stay ahead with the latest on compliance for India’s SaaS landscape

Get in touch!Q. What is the GST rate applicable to SaaS services in India?

SaaS services are generally subject to a GST rate of 18% in India. This applies to both domestic and imported services.

Q. How do I register for GST as a SaaS provider?

SaaS providers must apply for GST registration through the GST portal, submitting the necessary documents and details of their business operations.

Q. What are TDS implications for SaaS services provided by foreign entities?

TDS is applicable on payments made to foreign SaaS providers under Section 195 of the Income Tax Act. The rate varies based on the Double Taxation Avoidance Agreement (DTAA) provisions.

Q. What is the compliance burden for foreign SaaS providers in India?

Foreign SaaS providers must register for GST in India, comply with local tax laws, and file periodic returns to remain compliant

© 2025 Startup Movers Private Limited. All rights reserved. | Designed By : The Night Marketer